Subscribe

Personal Finance. Simplified

Helping you plan your finances better.

2nd

most influential

financial services brand

150,000+

Monthly readers

100,000+

Happy investors

17,000 Cr+

AUM Handled

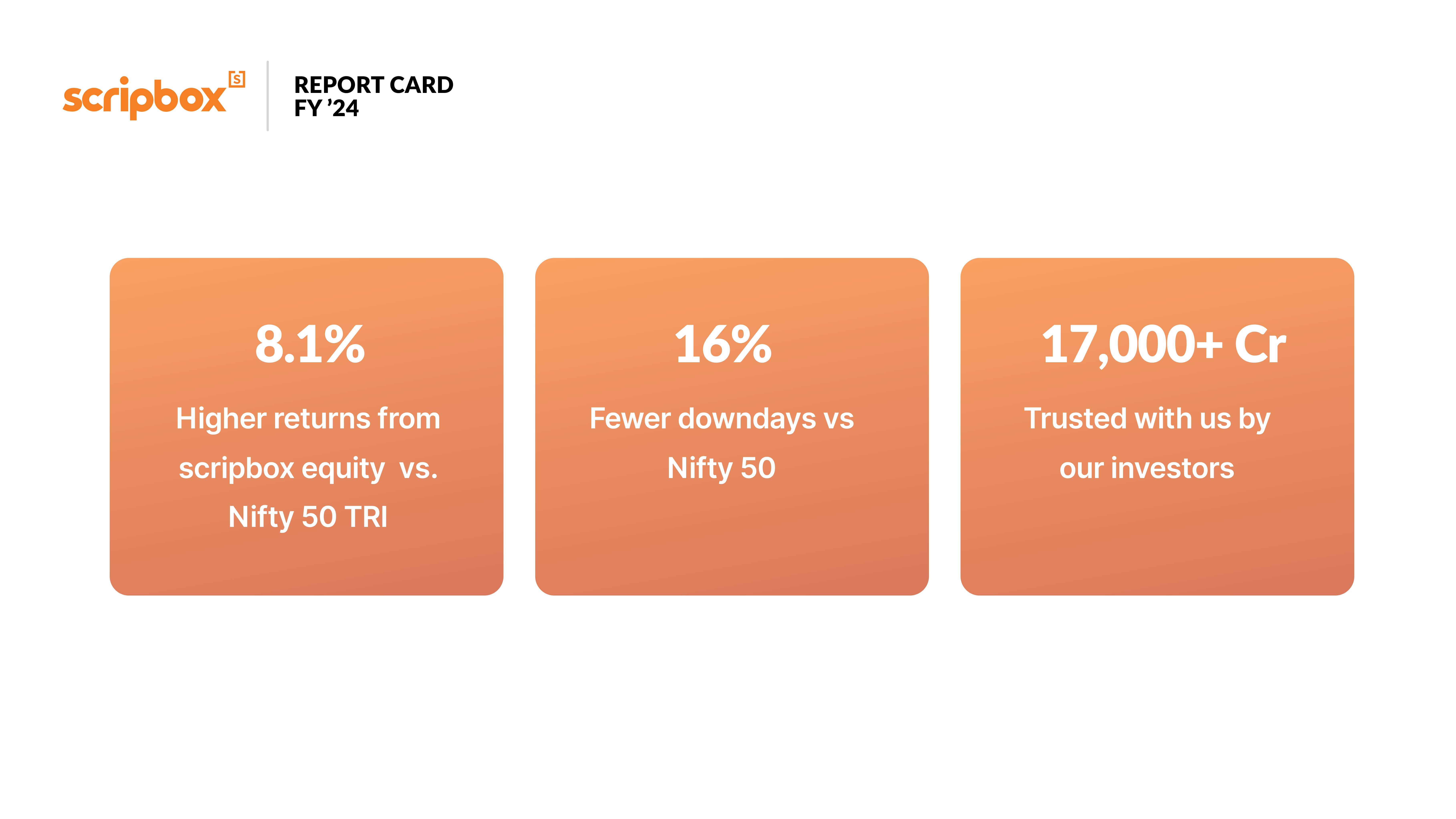

2023-24 Report Card: Performance of Scripbox Recommended Mutual Fund Portfolio

Family And Money

‘Are we sufficiently insured?’ The one conversation you must have with your spouse in your 40s

Action Plans

Financial checks to do on your 40th and 45th birthday

Editor's Picks

Popular Authors

Investment

Strategy

Personal

Finance

-

February 03, 2022

Citius, Altius, Fortius – Union Budget Highlights 2022

-

September 17, 2021

Why are Indian markets rising so much in 2022 and is it justified?

-

June 23, 2021

US Fed may hike rates. Will it impact Indian Equity?

Investing

Essentials

Trending Posts

Popular Categories

Our Finance Planners

Investment Strategy

- Why does it still make sense to invest in debt funds?

- Is it OK to invest in equity now, considering the market environment?

- With rates rising, are bank FDs back in vogue for your financial goals?

- An investor’s guide to investing in Target Maturity Funds – The debt fund that’s an index fund!

From the

Editor's Desk.

One home, and one app, for all your wealth

View, analyse, manage, and invest your and your family's wealth with the all-new Scripbox App.

One home, and one app, for all your wealth

View, analyse, manage, and invest your and your family's wealth with the all-new Scripbox App.