Share

Growing older comes with its joys and challenges. One of the most important things for seniors is keeping their money safe and growing. Finding the best saving schemes can help ensure a comfortable life after retirement. Several government investment schemes for senior citizens include the Senior Citizens Saving Scheme (SCSS), Post Office Monthly Income Scheme, and Senior Citizen Fixed Deposits (FDs). Let’s explore some top options, starting with a brief overview.

Best Senior Citizens Investment Plans with High Returns 2026

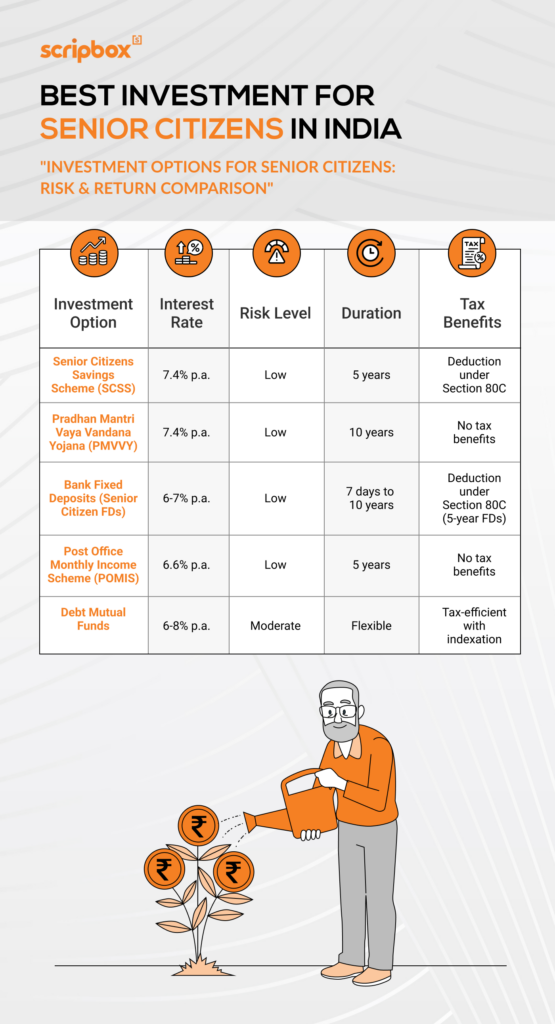

| Investment Option | Interest Rates | Minimum Investment Amount |

| Senior Citizens Savings Scheme (SCSS) | 8.20% p.a. | Rs. 1,000 |

| Post Office Monthly Income Scheme (POMIS) | 7.40% p.a. | Min Rs. 1,500 |

| Senior Citizen FD | 8.20% p.a. | Varies between banks |

| Tax-Free Bond | 5.5%-6.5% p.a. | NA |

| Mutual Funds | 12.00% to 30.00% p.a. | Rs.100 |

Let’s take a detailed look at some of the best investment plans for senior citizens.

Senior Citizens Savings Scheme (SCSS)

Senior Citizens Savings Scheme (SCSS) is one of the post office savings schemes for senior citizens. The Government of India backs the scheme. It offers safety and regular income through interest payments to its investors. The interest is computed every quarter and credited to the investor’s account. The interest rates are revised by the Ministry of Finance every quarter.

- Minimum Investment: INR 1,000

- Maximum Investment: INR 30,00,000

- Interest Rate: 8.20% p.a.

- Lock In Period: 5 Years

- Tax Saving: SCSS Investments qualify for tax deduction under Section 80C of the Income Tax Act, 1961

- TDS: The interest income is taxable, and a TDS is deducted if the interest is more than INR 50,000.

- Premature Withdrawal: Available, however, it attracts a penalty. Premature withdrawals are only allowed after one year of account opening. A 1.5% penalty is applied on the investment or deposited amount for withdrawals within two years of account opening. Also, a 1% penalty on the deposit amount is charged for withdrawals after two years of account opening. In the case of the account holder’s death before maturity, the account shall be closed, and the proceeds shall be given to the nominee or heir. Calculate SCSS returns.

Check Out PMVVY vs SCSS

What is SCSS?

The Senior Citizen Savings Scheme (SCSS) is a government-backed savings instrument designed specifically for senior citizens in India. Introduced in 2004, the SCSS aims to provide a steady and secure source of income for individuals above the age of 60. This long-term savings scheme offers a fixed interest rate, revised every quarter, ensuring a reliable income stream for its subscribers. The SCSS is an excellent option for senior citizens looking for a safe and dependable way to grow their savings.

SCSS Interest Rate

The current interest rate applicable to the SCSS is 8.2% per annum. This rate is effective from 1 April 2024 until 31 March 2025. The interest rate is determined based on several factors, including prevailing market rates and inflation levels. Once set, the interest rate remains fixed throughout the maturity tenure, providing stability and predictability for investors. Any changes in the interest rate in subsequent quarters will not affect the rate applicable to your SCSS account.

How SCSS Works?

The SCSS allows individuals to deposit a lump sum into the scheme, either individually or jointly, and receive regular income and tax benefits. Upon investing, the interest rate declared at the time remains fixed throughout the maturity tenure. The interest is compounded quarterly and disbursed every quarter on the first date of April, July, October, and January. This ensures a steady flow of income for the subscribers, making it a reliable option for senior citizens looking for consistent returns.

Account Opening Process

To open an account under the SCSS is easy. Here’s how you can do it:

- Visit a Bank or Post Office: Your account can be opened at any authorized bank or post office after filling out an application form.

- Provide Required Documents: You must submit proof of age, identity, address, and the form you have filled out.

- Make a Deposit: The minimum deposit is usually small, and you can deposit up to a certain limit.

- Collect Your Passbook: Once everything is done, you’ll receive a passbook for your account.

Eligibility Criteria

Before opening an SCSS account, make sure you meet the following requirements:

- Age: You should be 60 years or older. Some exceptions apply to those who have taken early retirement.

- Nationality: Only people who have Indian nationality can apply for this.

Documents Required to Open SCSS Account

To open an SCSS account, individuals need to provide the following documents:

- Proof of age (such as a birth certificate or PAN card)

- Proof of identity (such as an Aadhaar card or passport)

- Proof of address (such as utility bills)

- Proof of retirement (such as a retirement certificate)

These documents must be self-attested. Having all the necessary documents ready will make opening an SCSS account smooth and hassle-free.

The Senior Citizens Saving Scheme comes with many benefits:

- High Interest Rates: SCSS offers higher interest rates than regular savings accounts.

- Regular Income: Interest is paid out quarterly, providing a steady income.

- Safety: Being a government-backed scheme, your money is secure.

- Tax Benefits: You may get tax deductions on the amount you invest.

Post Office Monthly Income Scheme (POMIS)

India Post or the Department of Post (DoP) offers the Post Office Monthly Income Scheme (POMIS). The Government of India backs this savings scheme. POMIS is a low-risk investment option that offers depositors regular monthly income in interest payments.

- Minimum Investment: INR 1,000

- Maximum Investment: INR 9,00,000 per individual. INR 15,00,000 in case of a joint account.

- Interest Rate: 7.40% p.a.

- Lock In Period: 5 Years

- Tax Saving: Doesn’t qualify for tax deduction.

- TDS: No TDS.

- Premature Withdrawal: The scheme allows premature withdrawals after one year of account opening. However, premature withdrawals come with a penalty.

- Flexibility: POMIS account is transferable from one post office to another.

Senior Citizen FD

Senior citizen fixed deposits (FD) are traditional investment products. Bank fixed deposits offer a fixed return as they are the most preferred investment option. These are considered low-risk investments as the returns are guaranteed in the form of investment.

- Minimum & Maximum Investment: Varies from bank to bank

- Preferential Interest Rate: The FD interest rates ranges between 3%-7%. Senior citizens get up to 0.5% additional interest on their fixed deposits FD.

- Interest Payments: Senior citizenscan choose between getting interest payment regularly or at the time of maturity. For regular interest payments, they can choose between monthly, quarterly, half-yearly and annual intervals.

- Lock In Period: Depends don’t on scheme.

- Tax Saving: Investments in tax savings FDs qualify for tax deduction under Section 80C of the Income Tax Act, 1961.

- TDS: The interest income is taxable, and a TDS of 10% is deducted if the interest is more than INR 50,000.

- Taxation: The interest income is taxable at the individual investor’s income tax slab rate.

- Premature Withdrawal: Bank deposits are liquid investments as there is a premature withdrawal facility available with a penalty.

- Loan Facility: Available

Tax-Free Bond

Tax-free bonds are issued by government infrastructure organizations such as NTPC Limited, Housing and Development Corporation, NHAI, and Indian Railways Finance Corporation.

- Tenure: The tenure of the bond is above ten years.

- Lock-in Period: The investment has a lock-in period until maturity. Though there is a lock-in period, investors can sell the bonds on the stock exchange.

- Interest: The interest for these bonds ranges between 5.5%-6.5%. The bond issuer pays interest annually, and the entire interest amount is tax-free.

- Risk Free: Tax free bonds are low-risk investments as the schemes are backed by the Government. Hence the chances of default are low. Moreover, the scheme offers capital protection and promises regular income in the form of interest payments. Hence it is an ideal investment option for senior citizens.

- Taxation: The gains from the sale of bonds are taxable under Section 112. If the bond is sold before completing one year, the gains are taxable as per investor’s income tax slab rates. Suppose the bond is sold after one year. In that case, the long term capital gains will be taxable at 10% without indexation benefit and 20% with indexation benefit.

Explore our article on which is the best investment plan in india for middle class

Mutual Funds

Mutual funds are investment vehicles that pool money from multiple investors with similar objectives and invest in equities and debt securities. There are various categories of mutual funds, namely equity funds, debt funds, and hybrid funds. Equity mutual funds majorly invest in equities, while debt funds invest in debt and money market securities. Hybrid funds invest in both equity and debt securities. Senior citizens can align their goals with the fund’s objective and choose the right one.

In mutual funds, investors can not only invest monthly through SIP. They also have an option to withdraw their investments at regular intervals through SWP. Systematic Withdrawal Plans (SWP) allow investors to withdraw from their mutual fund investments regularly. Investors can withdraw a fixed or variable amount monthly, quarterly, half-yearly, or annually. Investors can withdraw just the capital gains, keeping their capital intact. Moreover, they must pay capital gains tax only on the withdrawn amount. Hence, SWP not only provides regular income but is also tax efficient.

Start Exploring Mutual Funds

Gold Mutual Funds

Gold has always been a favorite investment for many, especially senior citizens. Investing in gold mutual funds allows you to put your money into gold without buying and storing physical gold. These funds invest in gold bullion and gold-related securities, offering a simple way to add gold to your savings.

What Are Gold Mutual Funds?

Gold mutual funds are a type of investment where your money is pooled with others to invest in gold assets. The fund tracks the price of gold, so when gold prices go up, the value of your investment may increase, too.

Benefits of Investing in Gold Mutual Funds

- Easy to Buy and Sell: You can purchase gold mutual funds through banks or online platforms and sell them when necessary.

- No Storage Hassles: Since you’re not buying physical gold, you don’t have to worry about storing it safely.

- Diversification: Adding gold to your investments can balance your portfolio. Gold usually performs well when the stock markets fall.

Conclusion

The best investment schemes for senior citizens—such as the Senior Citizens Saving Scheme (SCSS), post office schemes, and senior citizen FDs—provide steady income and potential growth. Seniors can ensure a secure and comfortable retirement by choosing the right option among various government investment schemes for senior citizens, including gold mutual funds and the post office monthly income scent. Financial experts recommend making informed decisions based on individual needs.

Related Reads

1. Best Investment Plans To Invest in 2026

2. Best Investment Plan in India for Middle Class

3. Best Mutual Fund to Invest in India

5. Best Equity Mutual Funds to Invest in 2026

Frequently Asked Questions

According to Indian Law, a senior citizen is a person who is a citizen of India and has attained the age of sixty years or above. A person between the age of 60 years to 80 years is considered a senior citizen. And, above 80 years, they are known as super senior citizens.

The post office FD rates for senior citizens range from 6.90% to 7.50% p.a.. for the tenure ranging between 1 year to 5 years. The interest rate for the Senior Citizens Savings Scheme is 7.40% p.a.

You can invest in Senior Citizens Savings Scheme (SCSS), Post Office Monthly Income Scheme (POMIS), Senior Citizen FD, Tax-Free Bonds and Mutual Funds for regular monthly income during your retirement years.

The best way to make money at 80 is to generate regular income from your investments. It can get quite challenging to work at 80. Thus, you should aim to create an investment corpus that can support your expenses during retirement. Estimate your monthly expenses and determine how much corpus you would need to generate returns to support your monthly expenses. Use Scripbox’s Retirement Calculator to estimate your corpus amount.

Recommended Read: Short Term Investment Plans

Show comments