Share

Form 26QB is a payment challan which the buyer of the property needs to fill and submit to deposit the TDS amount. Income Tax Act, 1961 provides for deduction of TDS under section 194IA on purchase or sale of immovable property. In this article, we have covered all the aspects related to the requirement of Form 26QB, steps to fill and file Form 26QB, etc.

What is Form 26QB?

As per the provisions of section 194IA, when a buyer purchases an immovable property costing more than Rs. 50 lakhs, a tax at source is required to be deducted before making payment to the seller.

Form 26QB is a payment challan that is used by the buyer to deposit the tax deducted from the seller. The deductor/buyer can deposit the tax as per the below means:

- Pay the tax immediately online through the e-payment option

- Paying the tax later through the e-payment option or by visiting any of the authorized banks

Confused if your portfolio is performing right enough to meet your goals?

What are the Requirements of Section 194IA of the Income Tax Act?

As per the provisions of section 194IA, when a buyer purchases an immovable property costing more than Rs. 50 lakhs, a tax at source is required to be deducted before making payment to the seller. Immovable property includes building, part of a building, and land(other than agricultural land). Below are some of the features of section 194IA:

- The buyer shall deduct TDS before making payment to the seller. The tax rate of 1% is levied on the total sale consideration.

- No tax is deducted if the sale consideration is less than Rs. 50 lakhs.

- In case of payment by installments, tax has to be deducted on each installment.

- Consideration for the transfer of immovable property includes club membership fee, car parking fee, electricity and water charges, maintenance fee, or any other charges. The tax has to be deducted on the entire consideration @1%.

- The requirement of obtaining Tax deduction account number is not applicable to the person deducting the tax.

- The tax deducted at the source needs to be paid to the government within 30 days from the end of the month in which it was deducted.

- After depositing the tax to the government, the buyer shall furnish the TDS certificate to the seller in form 16B. The same can be obtained from the TRACES website.

- Tax is deducted at source @20% in case the seller does not provide PAN to the buyer.

Let us understand the applicability of section 194IA with the help of an example. Mr. Amit bought a house for Rs. 70 lakh from Mr. Ankit. Before making the sale consideration, Amit is required to deduct tax @1% on 70 lakhs amounting to Rs. 70,000.

How to Fill Form 26QB Online?

Below are the steps to pay the tax through challan 26QB:

Step 1: Log in to Official NSDL Website Under the ‘services’ tab click on e-payment: Pay Taxes Online. A new window will open as below.

Step 2: The taxpayer can click on TDS on property(Form 26QB)

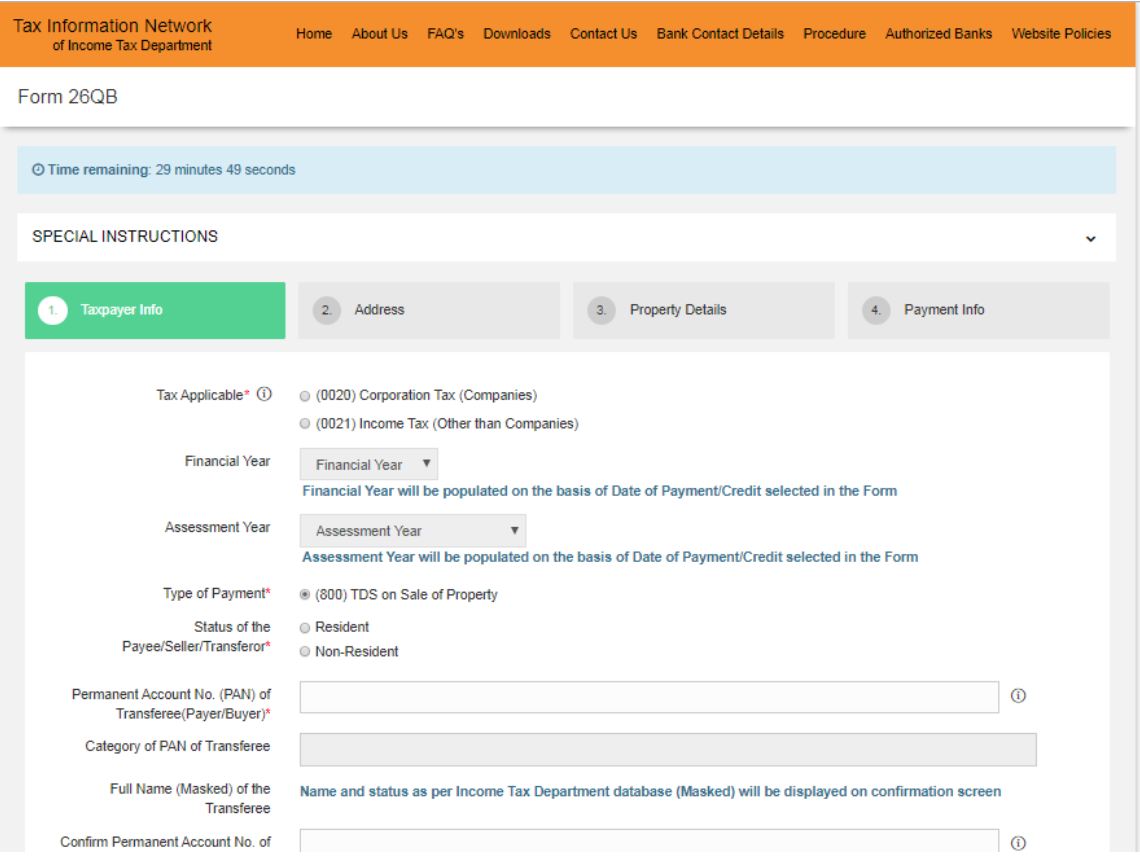

Step 3: Once the taxpayer click on ‘proceed’. A new window will open as shown below:

- In the tax applicable section, 0020 should be chosen if the taxpayer is a corporate payer and 0021 for a non-corporate payer.

- Other information such as residential status, PAN of the buyer, PAN of the seller, complete address of the property, tax amount to be deposited, etc

Step 4: Once all the relevant information is provided, there are two modes of payments- e-tax payment immediately (through net banking facility) and e-tax payment on the subsequent date (e-payment of taxes by visiting any of the Bank branches). The taxpayer can select one of the payment modes and proceed further.

- If the net banking facility is chosen, the taxpayer can log in to their net banking and pay online. Once the payment is successful, the bank allows the taxpayer to print the Challan 280.

- In the case of offline payment, an online receipt with a unique acknowledgment is generated. The taxpayer can pay at any of the authorized banks with the help of this challan.

What are the Steps to Register and Download Form 16B?

You must follow the following are steps that need to be followed by the taxpayer:

Step 1: For a first-time user, registration on the TRACES website is mandatory. The taxpayer should register as a taxpayer with the PAN and the challan number. The registration screen would look like below:

Step 2: Once the registration is complete, the taxpayer will be able to obtain Form 16B which can be issued to the seller. The seller can check the tax deducted in his Form 26AS within seven days of payment. The details will be reflected in the section “Details of Tax Deducted at Source on Sale of Immovable Property u/s 194(IA) [For Buyer of Property]”.

Step 3: In order to download form 16B, the taxpayer can log in to TRACES, and under the download tab, click on “Form-16B(for the buyer)” as shown below:

Step 4: the taxpayer needs to provide the details such as the PAN of the seller along with the acknowledgment number and click on proceed.

Step 5: Once the required information is entered, a request can be submitted to the department.

What are the Implications of Non or Late Filing of the TDS Statement?

Non-filing or late filing of the TDS statement will have an impact on the buyer and the seller. The impact on the buyer and the seller can be summarized as below:

- In the case of non/late filing of Form 26QB, a fee under section 234E will be levied on the taxpayer.

- In case of a continued failure, a fee of Rs. 200 shall be levied daily till the failure continues.

- A penalty under section 271H may also be imposed

- Buyer will be liable to pay interest on late deduction and deposit of tax

- In the case of non-deduction of tax, interest @1% per month shall be levied from the date of tax deduction to the date on which tax is actually deducted.

- In the case of non-deposit of tax, interest @1.5% per month shall be levied on which tax is deducted to the actual date of payment.

- The seller would not be able to claim the tax credit in the case of non/late filing by the buyer.

Frequently Asked Questions

Form 26QB is mandatorily required to be filed by the buyer for each seller irrespective of the share. For example, in the case of one buyer and two sellers, two Form 26QB are required to be filed.

As per the provisions of section 194IA, tax is required to be deducted on the entire amount paid to the seller. For example, if Mr. A purchased a property from Mr. B for Rs. 70 lakhs, Mr. A is required to deduct tax @1% on the entire consideration of Rs. 70 lakh and not the additional 20 lakhs (70lakh-50lakh).

For the purpose of tax deduction in accordance with the provisions of section 194IA, the Tax Deduction Account number is neither required by the buyer or the seller. It is however mandatory to quote the PAN of the seller at the time of tax deduction.

The PAN of the seller is mandatorily required to be obtained by the buyer and is required to be quoted in Form 26QB. It’s the buyer’s responsibility to arrange for the PAN of the seller.

Form 26QB is required to be filed on the purchase of property effected on or after 1st June 2013. Hence, there is no requirement to file form 26QB in case the formalities are completed before 1st June 2013.

Show comments