Share

Zero coupon bonds are fixed income securities that don’t pay any interest. At the time of maturity, the investor is paid the face value or par value. These bonds come with 10-15 years maturity. Hence, they trade at a deep discount. The bond pricing varies with time to maturity.

The higher the time until maturity, lower will be the price the investor will be willing to pay. These bonds best suit long term investment goals like retirement. However, these bonds trade on the stock exchange, and investors can sell them before maturity. In this article, we have covered all about zero coupon bonds.

What are Zero Coupon Bonds?

A coupon is an interest the bond issuer pays the bondholder. Coupon payments happen periodically from the time of issuance of the bond until its maturity. A zero coupon bond is a type of fixed income security that does not pay any interest to the bondholder. It is also known as a discount bond. These bonds are issued at a discount to the face value. In other words, it trades at a deep discount.

On maturity, the bond issuer pays the face value of the bond to the bondholder. Simply put, an investor gains from the difference between the buying price of the bond and its face value. Hence, there is no interest income from these bonds. The return an investor earns is the principal amount plus interest amount. The interest gets compounded semi-annually.

Zero coupon bonds are long term debt instruments. Hence investors who want to plan their retirement can invest in them.

Some bonds are issued as zero coupon bonds. In contrast, others transform into zero coupon instruments after a financial institution removes their coupons. Since zero coupon bonds pay the entire amount on maturity, the prices of the bonds tend to fluctuate more than coupon bonds.

Notified zero coupon bonds issued by REC and NABARD are taxable. Gains from zero coupon bonds are subject to capital gains tax on maturity. The capital appreciation for zero coupon bonds is the difference between the maturity price and purchase price of the bond. On the other hand, for non notified bonds, the difference between the maturity price and the purchase price is considered to be the interest. The interest is subject to taxation as per investor’s income tax slab rate.

Also Read: Best Bonds to Invest in India

How is the Price Calculated for a Zero Coupon Bond?

The price of a zero coupon bond is calculated using the YTM formula. If the above formula is rearranged to calculate for the price, then the market price of the bond will be:

Present value = (Face value /(1+YTM)^n) – 1

Let’s take an example of an investor who is expecting a rate of return of 6.5% from the bond with a maturity value (par value) of INR 1,000. The number of years until maturity is five.

The price the investor will be willing to pay would be

Price = (1000/(1+6.5%)^5) – 1

Present value or current market price would be INR 729.88. However, if the number of years until maturity are 3, instead of 5. Then the current market price would be INR 827.84.

Hence, the longer the time until maturity, the lower will be the price the investor will be willing to pay. This increases the return from investment in these bonds. Zero coupon bonds usually have longer maturities and can be useful for long term goals.

Also Read: Duration of a Bond

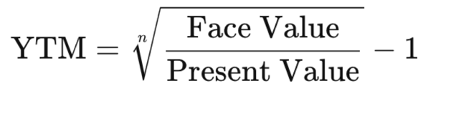

What is the Yield to Maturity for a Zero Coupon Bond?

Yield is a measure of all the cash flows of an investment over a period of time. It considers all the coupon payments and dividends received during the term of an investment. Yield to maturity (YTM) is the total return of an investment if it is held until maturity. Also, YTM accounts for the time value of money. It factors all the present values of future cash flows from an investment. This is the current market price of the bond.

YTM includes all coupon payments from an investment. But for a zero coupon bond, there are no coupon payments. The entire amount of money is received at the time of maturity. One can calculate the yield on them using the formula below.

Where,

Face value is the amount of money the investor receives upon maturity. It is the future value of the current price of the bond.

Present value is the current market price of the bond.

n is the number of years until maturity.

Also Read: Bond vs Bond Fund

Difference Between a Zero Coupon Bond and a Regular Bond

The significant difference between the zero coupon bond and a regular bond is the coupon payments. A regular bond pays interest to the bondholders. On the other hand, zero coupon bonds do not make any interest payments. The bondholders receive the face value (maturity value) of a bond upon maturity.

Regular bonds or coupon bonds pay interest throughout the life of the bond and also, the principal amount at maturity. One can calculate yield or rate of return by using the YTM formula. Also, the interest earned on these bonds is subject to taxation as per the investor’s income tax slab rate.

Therefore, regular bonds are suitable for investors seeking regular income during the tenure of their investment. In contrast, zero coupon bonds pay a lump sum amount on maturity (principal plus interest). They are suitable for a long term investment horizon as the investors need not worry about the changing market dynamics. Also, gains from these bonds are subject to capital gains tax on maturity.

Also Read: Bond vs Credit Funds

Advantages and Disadvantages of Investing in Zero Coupon Bonds

Advantages

Following are the advantages of zero coupon bonds

- Significant returns on maturity: These bonds are deep discount bonds that offer significant returns on maturity. Additionally, a bondholder can exit the bond by selling in the secondary market (stock market), in case the interest rates decline sharply.

- Fixed interest: These don’t offer periodic coupon payments. Thus there is no reinvestment risk of the coupon amounts. Moreover, the interest on them is assured.

- Long investment horizon: These bonds have a long investment horizon. Hence, they are suitable for long term investors. Investors can invest for a long term without worrying about the market turmoil or interest rate fluctuations.

Disadvantages

Following are the disadvantages of zero coupon bonds

- No regular income: These bonds do not offer periodic coupon payments. They provide a lump sum amount on maturity. Therefore, they are not suitable for investors seeking regular income. Investors seeking lump sum returns can consider these bonds for investing.

- Interest rate risk: Interest rates of these bonds may decline over time because of fluctuations in the market. Hence, investors selling the bond in the secondary market (stock market) are exposed to this risk. In other words, investors will have interest rate risk if they sell the bond before its maturity date.

Who Should Invest in a Zero Coupon Bond?

Zero coupon bonds do not pay any coupon or interest to its investors. Hence investors looking for regular income in the form of interest should consider interest-bearing bonds. Also, these bonds have a maturity of 10-15 years. They can be considered for long term financial goals like retirement, child’s education and marriage. Hence investors who want to invest for a long term with no regular income can consider these bonds. However, please note that most of these bonds are not inflation beating.

Also, these bonds are exposed to interest rate risk if sold before maturity. These bonds trade on the stock exchange. Hence investors can sell them before maturity.

Since the bonds are extremely sensitive to interest rate changes, they are exposed to duration risk as well. Therefore, investors who understand the risk can invest in them.

What is the Ideal Tenure for Zero Coupon Bond Investment?

Zero coupon bonds come with maturities of 10 to 15 years and are ideal for long term investment goals like retirement. The bond pricing varies with time to maturity. The market price of the bond is inversely related to the maturity of the bond. The longer the time until the maturity, the lower will be the price of the bond. This is because zero coupon bonds with a higher maturity period have more duration risk and interest rate risk than the one with lower maturity period. And the investors will want to pay a lesser price for the same. Hence these bonds offer deep discounts than any other short duration bonds.

How Does a Bond Coupon Work?

A coupon is a debt obligation of interest that the bond issuer has to pay to the bondholder. Usually, the coupons are described as coupon rate, i.e. the yield that the coupon bond pays from issuance date till maturity. The coupon rate is based on the face value of the bond at issue. Hence, a bond coupon rate is a fixed payment, meaning that it will remain the same for the lifetime of the bond. Typically, a coupon payment is made annually or semi-annually.

The coupon payments fluctuate due to the change in bond prices. In the rising interest scenario, the bond prices will fall. Therefore, the coupon payment becomes unattractive to the investors as they can sell the bonds with a low coupon rate. Also, they would prefer investing in another bond with a higher coupon rate. In a falling interest rate scenario, the bond prices can increase, causing the bond yield to fall. Here, the investor would want to profit from the price increase and sell the bond, leading to lower yields from the bond. Furthermore, once the investor sells the bond to earn profits, they will stop receiving coupon payments.

For example, if the bond’s face value is Rs.100, and it pays an interest of 8%. Here, the interest rate is the bond coupon.

Discover More

Frequently Asked Questions

When an investor purchases a bond, the bond issuer periodic interest payments known as the coupon rate. The bond issuer pays interest annually or semi-annually till maturity. Therefore, a 10% coupon bond means the bond issuer will pay a 10% coupon every year on the bond’s face value.

For example, The 10% coupon bond has a face value of Rs.1000 for 10 years. This means that the bondholder will receive Rs.100 every year for the next 10 years. The effective interest earned is 10%. Similarly, if the bond is bought above its face value, i.e. Rs.2000. The bondholder will still get Rs.100 only. Here, the interest earned would be only 5% ( Rs.100 of Rs.2000). Likewise, if the bond has been purchased below its face value, say Rs.500. The bondholder will continue to receive Rs.100 of coupon payment, but the interest earned would be 20% (Rs. 100 of Rs.500).

Confused if your portfolio is performing right enough to meet your goals?

- What are Zero Coupon Bonds?

- How is the Price Calculated for a Zero Coupon Bond?

- What is the Yield to Maturity for a Zero Coupon Bond?

- Difference Between a Zero Coupon Bond and a Regular Bond

- Advantages and Disadvantages of Investing in Zero Coupon Bonds

- Who Should Invest in a Zero Coupon Bond?

- What is the Ideal Tenure for Zero Coupon Bond Investment?

- How Does a Bond Coupon Work?

- Frequently Asked Questions

Show comments