Subscribe

Personal Finance. Simplified

Helping you plan your finances better.

2nd

most influential

financial services brand

150,000+

Monthly readers

100,000+

Happy investors

18,500 Cr+

AUM Handled

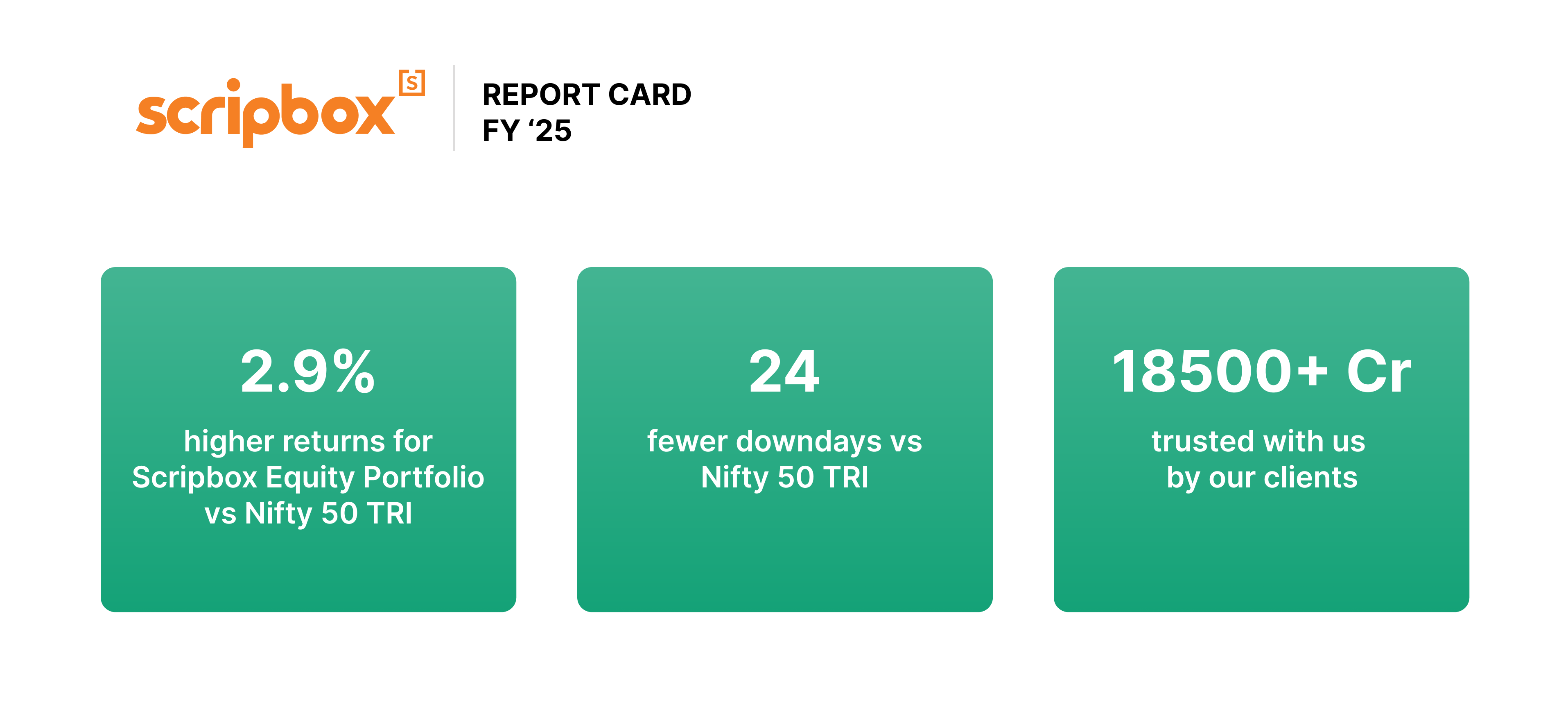

Report Card

2024-25 Report Card: Performance of Scripbox Recommended Mutual Fund Portfolio

We heard you! Your Scripbox app is changing for the better.

Armed forces personnel? Know what is commutation & how should you invest your commutation lumpsum.

From the

Editor's Desk.

Our Finance Planners

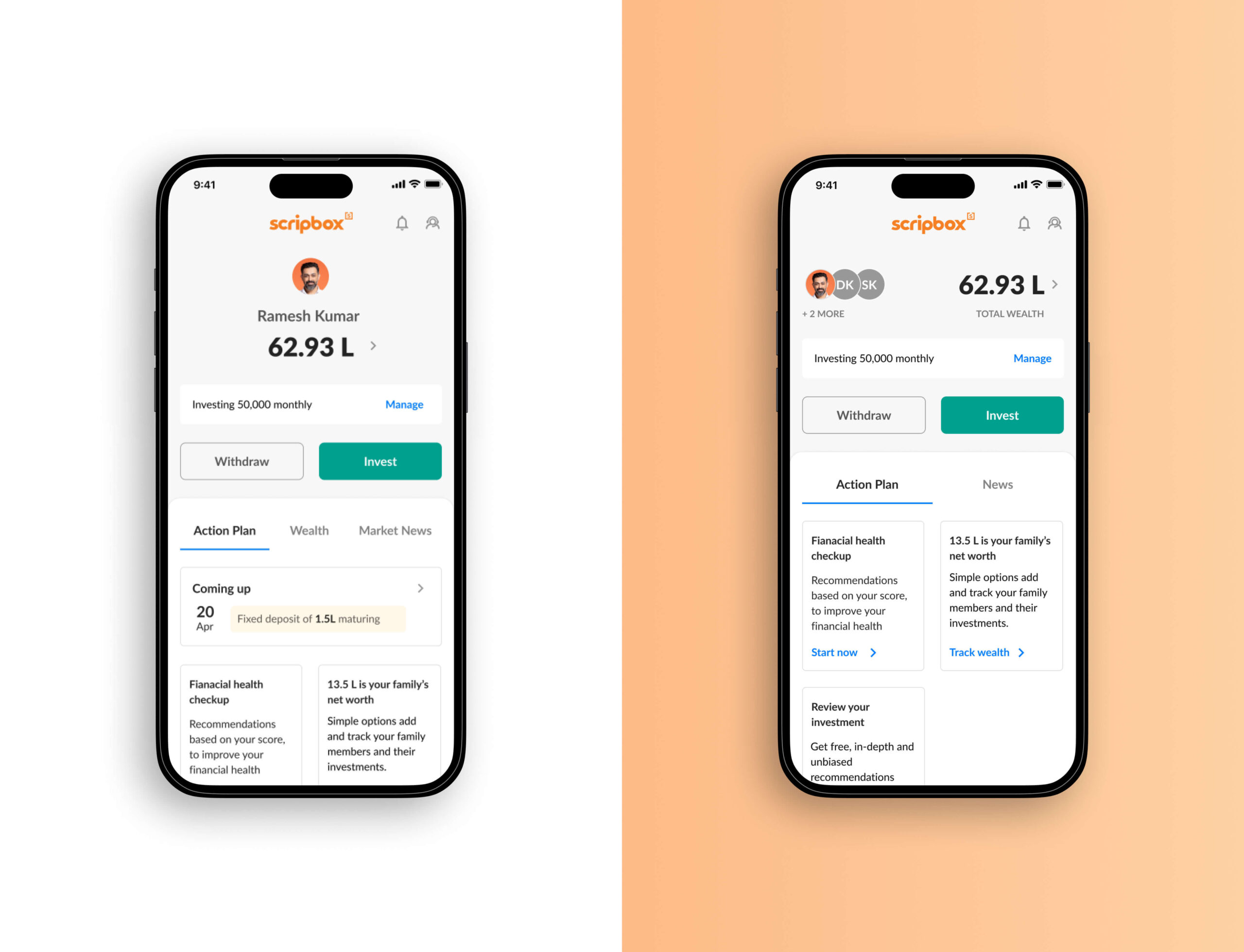

One home, and one app, for all your wealth

View, analyse, manage, and invest your and your family's wealth with the all-new Scripbox App.

One home, and one app, for all your wealth

View, analyse, manage, and invest your and your family's wealth with the all-new Scripbox App.