Share

A huge car, a luxurious home, lavish holidays and a cushy retirement — can you imagine a better life for yourself? All this means you should either have a very large income or a very good plan to meet all these goals, and the best time to start is when you are just starting your first job.

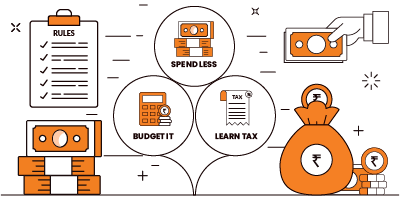

The Golden Investment Rules For First Time Jobbers

By following these three simple investing rules for first time investors, you can save and make a lot of money by investing, so your salary is not your only source of income.

1. Spend less than you earn

Everyone knows that spending more than what you earn will only leave you in crippling debt in the future. Spending exactly how much you earn means you won’t have any money to tide you over in bad times. If you learn to spend less than your income, and these savings go to smart investments, you stand a chance of having a comfortable future.

2. Budget it

The first step is to record all your income and expenses. See where your money is coming in from and where it’s all going. Once you’re able to classify how much you spend on essentials and how much goes to entertainment and the like, you will be able to cut down on the extras and plan your money better.

Put away 10–20% of your salary the second you receive it, so that you will always have that money available in case of a rainy day.

3. Learn about tax

Learning where and how much your income is going to be taxed is an important skill to have. Though this may not be a large concern to you right now, if you’re earning enough to even make the first tax slab, it will definitely make a difference when your salary increases and you’re not sure why you’re paying so much of it back.

Find instruments that give you tax benefits, such as tax saving mutual funds, get exemptions under section 80C and minimize the amount that you are required to pay back.

*All returns are indicative basis past performance. Actual performance can vary.*

Show comments