Share

Budget 2023 Updates

The amount of advance tax paid is reduced only once for computing the interest payable u/s 234B if the taxpayer files an updated ITR.

Advance tax is paid on income that one earns during the year, usually in installments. It is estimated based on the income that one might earn during the year. Anyone with a tax liability above INR 10,000 is liable to pay advance tax.

Confused if your portfolio is performing right enough to meet your goals?

What is advance tax?

Advance tax means advance payment of Income Tax instead of paying a lump sum at the year-end. Also, it is known as pay as you earn tax. Furthermore, the assessee has to make these payments in installments as per the due dates provided by the Income Tax department.

It is the income tax one has to pay if their total tax payable or liability exceeds INR 10,000 in a financial year. It has to be paid in the year in which the income is received.

Advance tax collection is to ensure that the government is able to collect taxes uniformly throughout the year. For example, the government collects TDS from individuals. However, some individuals who do not fall under the tax bracket can claim a tax refund for the TDS. Similarly, in some cases, the TDS might be lesser than the total tax liability. In such cases, it has to be deposited.

The taxpayers can pay either online or offline. To make an offline transaction you must use the tax payment facility at the authorized bank branches. A taxpayer can pay it online through the National Securities Depository Ltd (NSDL) website.

Who is liable to pay advance tax?

Salaried individuals, freelancers, and businesses

If the total liability in a financial year is more than INR 10,000, then the taxpayer has to pay advance tax. All taxpayers including freelancers, salaried, businesses are liable to pay advance tax. An exception has been given to senior citizens who are above the age of 60 years. The senior citizens who do not run a business are exempt from advance tax.

Presumptive income for Businesses

Few taxpayers opt for the presumptive taxation scheme under section 44AD. Such taxpayers are liable to pay the entire amount of advance tax in one installment on or before 15th March. These taxpayers have an option to pay their total tax liabilities by 31st March.

Presumptive income for Professionals

Professionals such as lawyers, doctors, architects, etc., opt for presumptive income under section 44ADA. Such taxpayers are liable to pay the entire amount in one installment on or before 15th March. These taxpayers have an option to pay their total tax liabilities by 31st March.

Exemption to Senior citizens from advance tax payment

With an aim of making tax compliances easier for senior citizens, the Income-tax Department in the FY 2012-13 ratified section 207. As a result, the senior citizens are not liable to pay advance tax on fulfillment of the below-mentioned conditions:

- The taxpayer is more than 60 years of age

- The individual is a resident of India

- A taxpayer does not hold any income under the head ‘business or profession’

- The taxpayer is an existing senior citizen at any time during the financial year. For example- in case you have attained the age of 60 years during the financial year, you will still be exempt from advance tax.

How to Calculate Advance Income Tax Payment? Explained with an Illustration

You can estimate your advance income tax liabilities by following the 4 simple steps

- Estimate your income to be earned during the financial year

This includes estimating income that one might receive during the year. Income from interest, professional income, capital gains, rent, etc. have to be clubbed together.

- Estimate the expenses related to the estimated income

- Estimate the deductions you will claim under Chapter VIA.

- Calculate the total tax liability

While calculating the tax liability ensure that you take into account:

- The slab rate applicable to you

- Tax rebate u/s 87A

- The TDS to be deducted by other taxpayers on your income

Let us understand the entire process with the help of an example

Mr. Arun is a taxpayer who earned income under the head ‘Business and Profession’.

Estimated Gross Receipts for the financial year- Rs 22,00,000

Estimated Expenses related to income earned- Rs 10,00,000

Receipts on which TDS is expected to be deducted- Rs 4,00,000

Interest Income- Rs 50,000

Let us calculate the liability now:

| Particulars | Amount (Rs) | Amount (Rs) |

| Gross Receipts for the financial year | 22,00,000 | |

| Expenses related to income earned | 10,00,000 | |

| Income From Profession | (22,00,000 – 10,00,000) | 12,00,000 |

| Income From Other SourcesInterest on Fixed Deposit | 50,000 | |

| Total Income Chargeable to Tax | 12,50,000 | |

| Less: Deductions under Chapter VIA | ||

| Investment in PPF Account | 50,000 | |

| Investment in ELSS Mutual Funds | 70,000 | |

| Investment in Tax-Saving Fixed Deposit | 30,000 | |

| Deduction under Section 80D | 30000 | 1,80,000 |

| Total Taxable Income | 10,70,000 | |

| Tax Payable | 1,33,500 | |

| Less: TDS Deducted by other taxpayers | (4,00,000 * 10%) | 40,000 |

| Tax Payable in Advance | 93,500 |

Advance Tax Payment Installments and Due Dates

| Due Date | Advance tax installment | Amount (Rs) |

| 15th June | 15% of Advance tax | 14,025 |

| 15th September | 45% of Advance tax | 42,075 |

| 15th December | 75% of Advance tax | 70,125 |

| 15th March | 100% of Advance tax | 93,500 |

Advance Tax Due Dates

It is vital to pay advance tax on or before its due date. Non-timely payments attract interest and penalty at the time of filing annual income tax returns. Following are the advance tax due dates for corporate taxpayers, self-employed, and businessmen:

| Advance Tax Due Date | Advance Income Tax Instalment Amount |

| On or before 15th June | 15% of advance tax liability |

| On or before 15th September | 45% of advance tax liability less advance tax already paid |

| On or before 15th December | 75% of advance tax liability less advance tax already paid |

| On or before 15th March | 100% of advance tax liability less advance tax already paid |

For taxpayers who opted for presumptive taxation scheme u/s 44AD and u/s44ADA of the Income Tax Act, the following is the advance tax payment due date:

| Advance Tax Payment Due Date | Advance Tax Instalment Amount |

| On or before 15th March | 100% of advance tax liability |

What is the penalty for non-payment of the advance tax?

Non-payment of advance tax attracts an interest u/s 234C. The interest is charged @ 1% from the due date of individual installment till the date of actual payment. In the table below we have explained the interest chargeable along with the calculation of interest.

For taxpayers who have not opted for presumptive income

| Simple Interest | Period of Interest | Amount on which interest is calculated | |

| If Advance Tax paid on or before June 15 is less than 15% of the Net Amount* | 1% per month | 3 months | 15% of Net Amount* (-) tax deposited before June 15 |

| If Advance Tax paid on or before September 15 is less than 45% of Net the Amount* | 1% per month | 3 months | 45% of Net Amount* (-) tax deposited before September 15 |

| If Advance Tax paid on or before December 15 is less than 75% of Net Amount* | 1% per month | 3 months | 75% of Net Amount* (-) tax deposited before December 15 |

| If Advance Tax paid on or before March 15 is less than 100% of Net Amount* | 1% per month | – | 100% of Net Amount* (-) tax deposited before March 15 |

Net Amount = Tax liability on total income chargeable to tax (-) tax paid

Tax Paid in terms of relief, TDS, TCS, or Tax Credit

How to pay advance tax online?

Advance tax payment can be made offline with any of the authorized bank branches approved by the Income Tax Department. Alternatively, one can make an advance tax payment online.

Below are the steps for payment of advance tax online:

- Visit the Tax Information Network website at https://onlineservices.tin.egov-nsdl.com/etaxnew/tdsnontds.jsp

- Click on ‘Proceed’ under ‘Challan No./ITNS 280’ under ‘Non TDS/ TCS’

- Enter the information on the screen to generate the challan

- Tax Applicable

For Companies- select ‘(0020) Corporation Tax (Companies)’

For Other than Companies- select ‘(0021) Income Tax (Other than Companies)’

- Type of Payment

Among the options listed select ‘(100) Advance Tax’ for payment

- Mode of payment

Select the mode of payment, you can pay either through net banking or debit card. In both cases, you will have to select the ‘Bank Name’ from the drop-down menu.

- Enter your Permanent Account Number PAN

- Enter the Assessment Year. Select the assessment year very carefully. An incorrect AY would need a rectification by applying to the assessing authority. Be very careful to avoid any hassle.

- Enter your address with city/ district, state, and PIN Code being mandatory fields and your email ID and mobile number

- Enter the captcha code displayed on the screen

- Click on Proceed

- You will be to the bank’s website to complete the transaction

- After completing the payment, you will receive the bank receipt. The bank receipt will contain the BSR code and challan serial number. You must save the challan copy for future reference.

How to claim the advance tax paid while filing ITR?

You can claim the advance tax paid while filing your income tax return. You can file your ITR either offline or online.

Online Filing of ITR

When you opt for online tax filing under the ‘Prepare and Submit’ option, all your transactions will be pre-filed. These details are available to the income tax authorities in the form of transactions made by you or by other taxpayers on your behalf. Whenever any transaction takes place on your PAN, it gets recorded and mapped to PAN and consequently pre-filled in your ITR.

Hence, the advance tax payment details will be pre-filed. You only need to check the information and proceed.

Offline Filing of ITR

- In case you have selected the Offline ‘Download and Prepare’ option, you will have to fill in the details manually.

- Go to the third tab ‘TDS’ and scroll down to item 21

- Under item 21 ‘Details of the Advance tax and Self Assessment Tax payments’ enter the below details. You will find all the details in the challan itself

- BSR Code

- Date of Deposit

- Serial Number of Challan

- Tax paid

- Go To the fourth tab of the utility ‘Tax Paid and Verification’.

- Enter the amount of tax paid under ’Total Advance Tax Paid’. Ensure that the details filled under ‘Item-21’ match with ’Total Advance Tax Paid’.

How to check advance tax payment status?

You can check the status either through Form 26As or by visiting the NSDL website.

Form 26AS

- Login to your account through the incometaxindiaefiling website

- Go To ‘My Account’. From the dropdown menu, click on ‘View Forn 26AS tax Credit’

- Click on ‘View Form 26AS’

- You will be asked for confirmation to be redirected to the Traces website or TDS CPC website. This redirection to the Traces website is a necessary step. It is completely safe as the Traces website is regulated by the Government of India

- Select the box on the screen and click on the ‘proceed’ CTA

- You find an option at the bottom of the page. Click on the ‘Click View Tax Credit (Form 26AS) to view your Form 26AS’ option

- You will land on the ‘View Tax Credit (Form 26AS)’ page. Here you can simply view Form 26AS or download a PDF file

- You can view all the TDS deducted and advance tax paid details in the Form 26AS

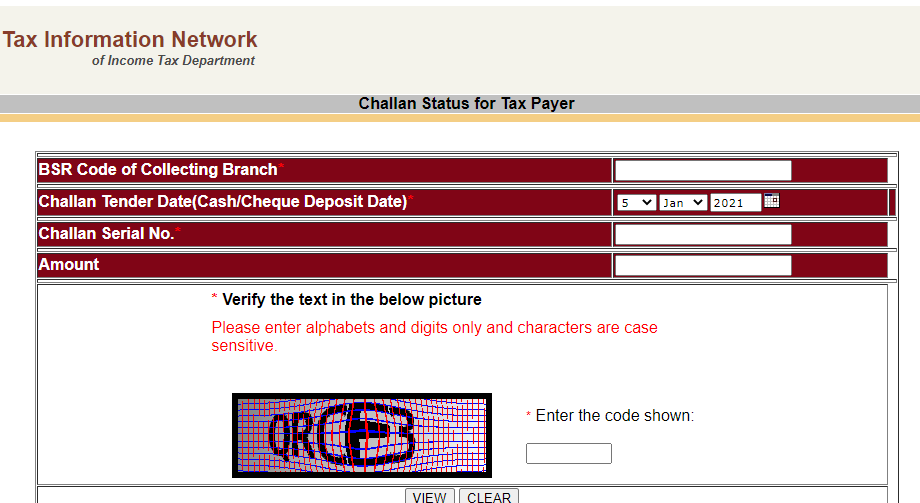

Through NSDL website

- Visit the website by clicking on this link

- Select ‘CIN based View’

- Enter the below details. You can find these details in the bank receipt you received while making the payment.

- BSR code of the collecting bank

- Challan Tender Date or Challan Deposit Date

- Challan Serial Number

- Amount

- Enter the captcha code and click on ‘View’. You will be able to check the status of your payment here.

Related Articles

- What is advance tax?

- Who is liable to pay advance tax?

- How to Calculate Advance Income Tax Payment? Explained with an Illustration

- Advance Tax Due Dates

- What is the penalty for non-payment of the advance tax?

- How to pay advance tax online?

- How to claim the advance tax paid while filing ITR?

- How to check advance tax payment status?

Show comments