Sometimes, it is possible that once the taxpayer files their income tax return, the assessing officer finds some errors in the assessment. In such cases, the mistakes that are apparent from the record can be rectified by the taxpayer under section 154 of the Income Tax Act, 1961.

Once the taxpayer files the return, the department compares the information in the return with the information it posses. Upon comparison, if there is any mismatch between the two sets of data then the department will inform the assessee via an intimation. The assessee can either agree or disagree with the calculations provided in the intimation shared by the department. You can find the following issues in the intimation:

- Higher demand by the department.

- Higher refund claimed by the assessee.

If the assessee agrees with the demand raised by the department, they can pay the demand. If the assessee feels that the data is incorrect, they can file a rectification request under section 154 of the Income Tax Act, 1961.

Which Orders Can Be Rectified Under Section 154 of the Income Tax Act, 1961?

In order to rectify any mistakes apparent from the record, you can do the rectification for the following orders:

- An order passed under any provisions of the income tax act.

- Intimation or deemed intimation under section 143(1)

- An intimation under section 200A(1) [TDS returns]

- Intimation under section 206B [TCS statement]

Below are a few examples of the mistakes apparent from records:

- Treatment of a non-agricultural income as agricultural income.

- A subsequent judgment passed by the Supreme Court

- Any retrospective amendment in the law.

What Are the Features of Section 154?

The following are a few features of section 154 of the Income Tax Act, 1961:

- the department can make the rectification suo moto or on the basis of the application filed by the assessee.

- The Income Tax Department must complete the rectification requests within 6 months. The period of 6 months starts from the end of the month the Income Tax Department receives the application.

- In case the rectification is taken up by the department, the same can be made up to 4 years from the end of the financial year in which the order rectified is to be passed.

- If rectification results in additional tax liability or reduction of refund for the assessee then he/ she will have an opportunity of being heard.

What Errors can be Rectified by Filing by Rectification Request?

You can make a rectification request under section 154. The request will be for the mistakes which are apparent from records in the income tax return. The following are some errors that can be rectified by filing a rectification request:

- Any arithmetical mistake in the income tax return

- Any error of fact

- Clerical error

- Error caused by omitting to consider the compulsory provisions of the law

Examples of the above can include but are not limited to cases such:

- as a mismatch in the tax credit claimed by the taxpayer

- mismatch in the advance tax paid by the taxpayer

- missing details with respect to any transaction which is compulsory at the time of filing of the income tax return.

By When Can You File A Rectification Request?

The taxpayer can file a rectification request under section 154 only after the processing of the return. The Income Tax Department is responsible for the processing of the income tax return. While filing a rectification request, a taxpayer cannot claim any new deductions or exemptions. If the taxpayer believes that making the changes would lead to an increase in the total income, he must file a revised return instead of a rectification request.

What are the Steps to File a Rectification Request Online?

The following are the steps you must follow to file a rectification request under section 154 online:

Step 1: Log in to the income tax website.

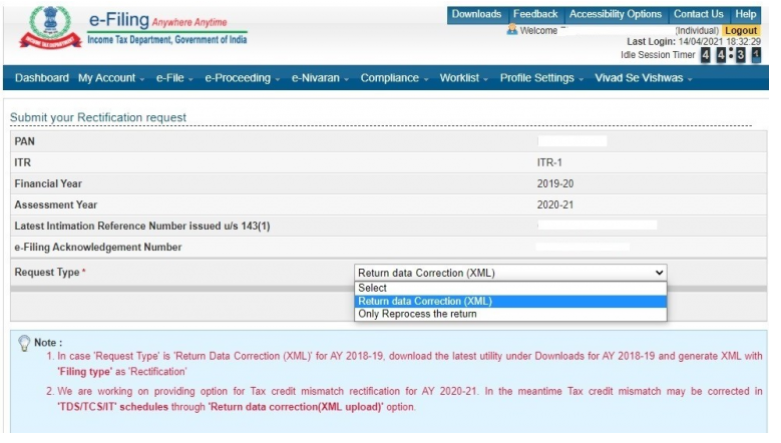

Step 2: Go to the ‘e-file’ option. Under the drop-down menu, select ‘rectification’. The screen would look like below:

Step 3: Select the ‘Order/ Intimation to be rectified’ as ‘Income Tax’. Select the relevant assessment year for which you want to file the rectification. Click on continue.

Step 4: In the next screen, select the request type as Return data Correction or Only Reprocess the return as applicable.

Upon clicking on Return data Correction, the taxpayer can select a maximum of 4 reasons:

The taxpayer needs to select the reason for which they seek rectification. Then add the schedules in the returns that will be changed. Next, you need to upload the XML.

Only Reprocess the return: A taxpayer can select this option in case of only reprocessing of return. In this case, you do not need to upload the income tax return.

Step 5: Upon successful completion and submission of the request, the department will generate a reference number. Such a reference number is sent to CPC Bangalore for further processing.

What are the Time Limits for Rectification Under Section 154?

The time limit for rectification under section 154 of the Income Tax Act, 1961 falls under the following 2 categories:

Category 1: Where the assessee or deductor makes an application. The time limit is 6 months from the end of the month in which the department receives the application.

Category 2: If the department takes up a Suo moto rectification. The time limit is four years from the end of the financial year in which the order sought to be amended was passed by the department.

What is the Procedure for Making an Application for Rectification?

The taxpayer needs to keep the following points in mind before filing the application for rectification under section 154 of the Income Tax Act, 1961:

- taxpayer should carefully study the order against which they are filing the rectification.

- taxpayer should be careful of the calculations they are making. At times the calculations made by the taxpayer are incorrect as compared to the ones made by the department. In this case, the CPC system would have corrected the calculations and the intimation shared with the taxpayer would reflect the correct calculations.

- If the taxpayer identifies the mistakes which are genuine and the calculation is correct, they can proceed with filing a rectification request. They can file the rectification request online with the department.

- Only the mistakes that are apparent from records should be considered while filing the rectification request under section 154. The mistakes that require further clarification, or are debatable should not be considered.

What is the Difference between Rectification and Revised Return?

A taxpayer files a revised return in order to make changes to the original return. This can include any omission of income or any wrong statement. They can file a revised return at any time before the end of the relevant assessment year. A revised return can be filed multiple times within the given time limit.

A taxpayer can file the rectification request or it can be taken up suo moto by the department. A rectification request aims to rectify the mistake apparent from records. The department needs to dispose of the rectification request filed by the assessee within 6 months from the end of the month in which the application is received. In case the rectification is taken up by the department, the same can be made up to 4 years from the end of the financial year in which the order rectified is to be passed.

Frequently Asked Questions

The taxpayer can make an application online to intimate the department of the mistake and request for the rectification of the same. Furthermore, the income tax department can rectify the mistake on its own.

An order cannot be rectified under section 154 if the same has been a subject matter of any apparel or revision and is decided in such appeal or revision. Only the matter that has not been decided by the authority can be rectified under section 154 of the Income Tax Act, 1961.

The taxpayer has to make a rectification request to the department. Upon receipt of the application, the income tax department shall amend the order within 6 months from the date of receipt.

The amendment can have the effect of either increasing the income or reducing the refund amount payable to the taxpayer. The department can’t process the changes till the taxpayer has been given notice of their intentions to make the changes. The assessee shall be given a reasonable opportunity to being heard.

Popular Income Tax Sections

Related Articles

- Which Orders Can Be Rectified Under Section 154 of the Income Tax Act, 1961?

- What Are the Features of Section 154?

- What Errors can be Rectified by Filing by Rectification Request?

- By When Can You File A Rectification Request?

- What are the Steps to File a Rectification Request Online?

- What are the Time Limits for Rectification Under Section 154?

- What is the Procedure for Making an Application for Rectification?

- What is the Difference between Rectification and Revised Return?

- Frequently Asked Questions